In today’s evolving mortgage market, Conventional Rate & Term Refinance campaigns are gaining serious traction among direct-to-consumer lenders.

Why? Because the data shows these campaigns deliver strong borrower engagement, high-quality leads, and some of the lowest acquisition costs in the industry.

At Monster Lead Group, we’re seeing lenders lean heavily into this strategy—and for good reason.

In this breakdown, we’ll walk through:

- What a Conventional Rate & Term Refinance is

- Why borrowers pursue it

- Key performance metrics from active campaigns

- How loan officers can identify ideal candidates

If you’re looking to generate higher-quality refinance opportunities, this is a program worth understanding.

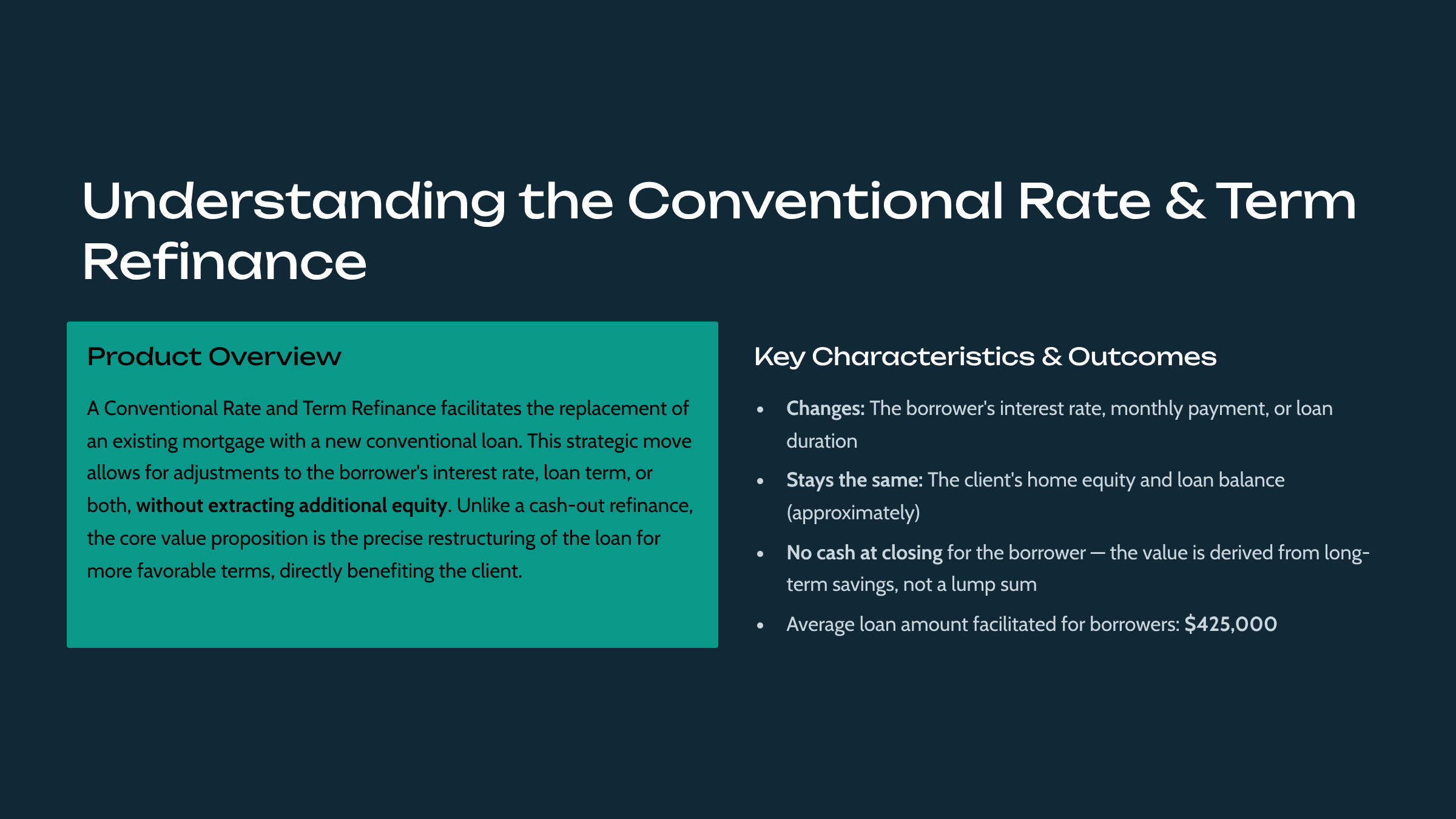

What Is a Conventional Rate & Term Refinance?

A Conventional Rate & Term Refinance replaces a borrower’s existing mortgage with a new conventional loan that offers improved terms.

The goal is simple: optimize the structure of the loan without tapping home equity.

Unlike a cash-out refinance, this program focuses entirely on improving the borrower’s mortgage terms.

What Can Change

- Interest rate

- Monthly payment

- Loan term (shorter or longer)

What Typically Stays the Same

- The borrower’s home equity

- The loan balance (approximately)

In other words, borrowers are not receiving cash at closing. The value comes from long-term savings and improved financial stability.

Across active campaigns, the average loan amount for borrowers pursuing this refinance is approximately $425,000.

Why Borrowers Choose a Rate & Term Refinance

Most borrowers pursue this strategy for one of two reasons: saving money or gaining financial stability.

1. Lower Interest Rate & Monthly Payment

When mortgage rates drop below the borrower’s original loan rate, refinancing can significantly reduce:

- Monthly mortgage payments

- Total interest paid over the life of the loan

For many homeowners, this creates meaningful long-term savings.

2. Converting an ARM to a Fixed Rate

Borrowers with Adjustable-Rate Mortgages (ARMs) often refinance to lock in a fixed interest rate.

This removes the uncertainty of future rate increases and provides predictable monthly payments for the life of the loan.

Why ARM-to-Fixed Conversions Are Increasing

Many homeowners currently holding ARMs are facing potential payment volatility as rates fluctuate.

Refinancing into a fixed-rate conventional mortgage allows borrowers to:

- Eliminate future rate adjustment risk

- Stabilize monthly payments

- Plan long-term household finances with confidence

For loan officers, these borrowers often represent some of the most motivated refinance candidates in the market.

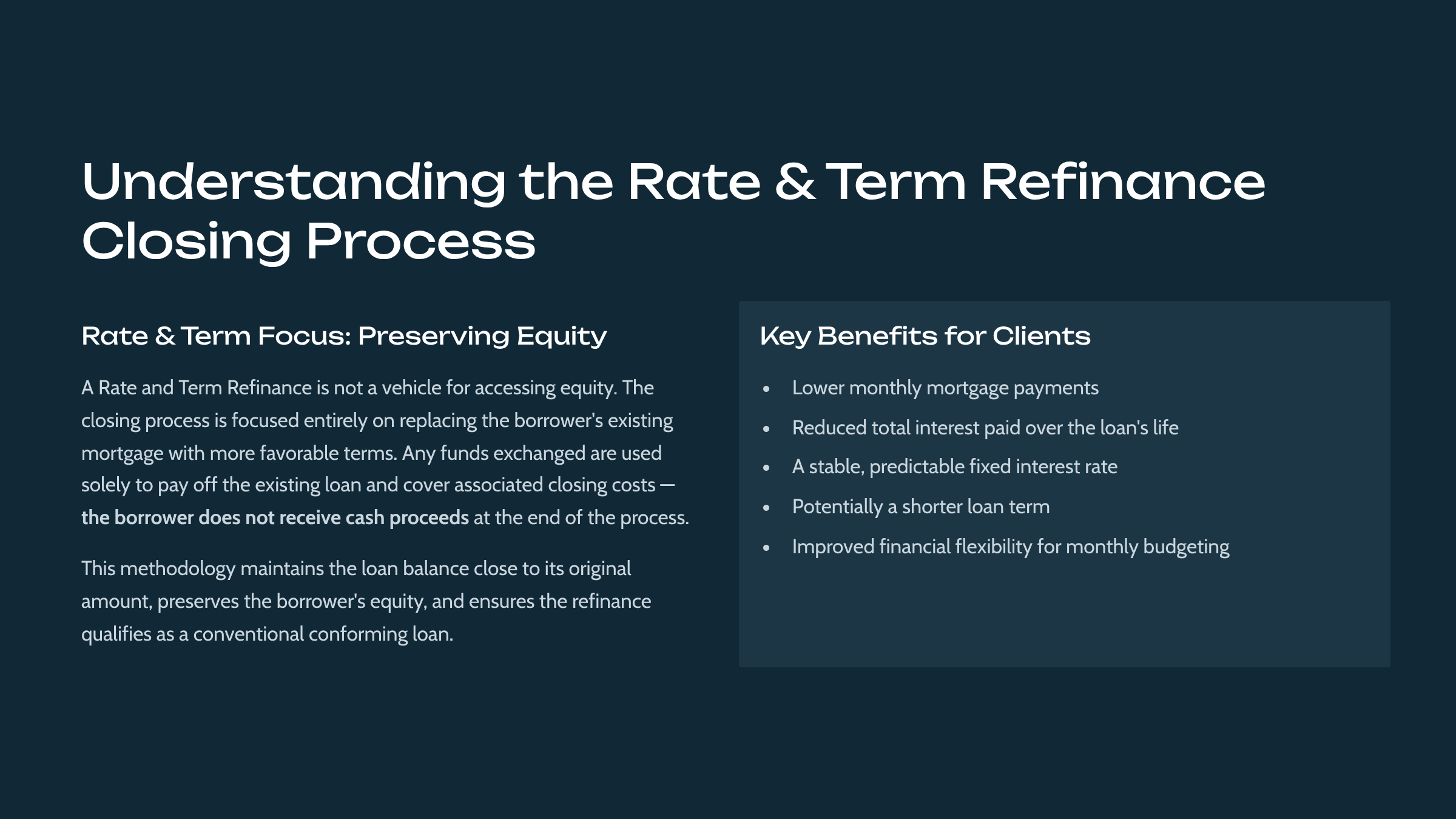

How the Rate & Term Refinance Process Works

A key distinction with this refinance strategy is that it preserves the borrower’s home equity.

During closing:

- The new loan pays off the existing mortgage

- Funds are used to cover closing costs

- No cash is distributed to the borrower

This structure ensures the loan remains conventional and conforming, while focusing entirely on improving loan terms.

Key Borrower Benefits

- Lower monthly mortgage payments

- Reduced total interest paid over time

- A predictable fixed interest rate

- Potentially shorter loan terms

- Greater financial flexibility for budgeting

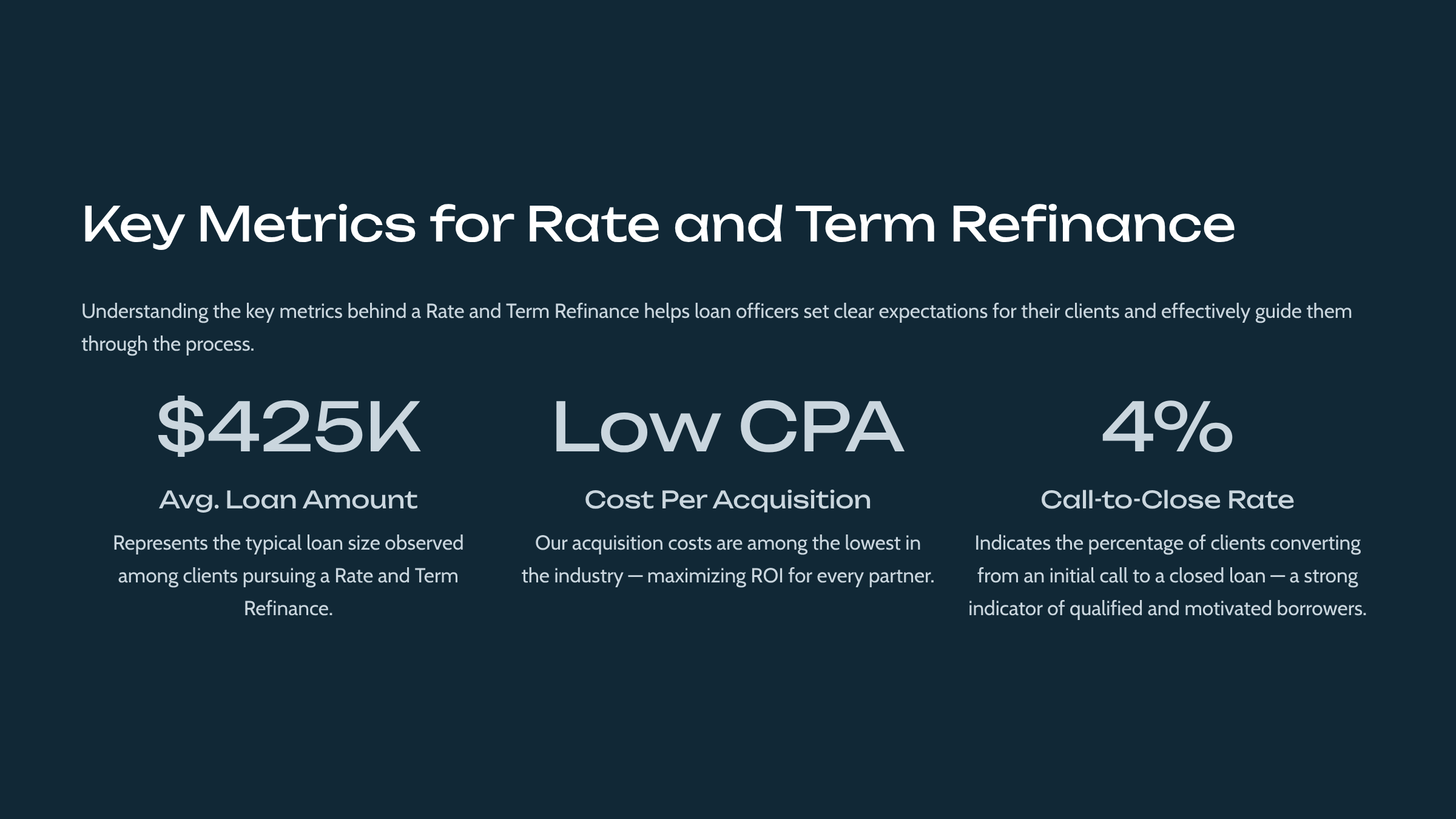

Key Metrics From Active Campaigns

Lenders actively running Rate & Term Refinance campaigns are seeing strong performance metrics.

$425K Average Loan Amount

Typical loan size among borrowers currently pursuing rate-and-term refinances.

4% Call-to-Close Rate

Approximately 4 out of every 100 borrower consultations convert to closed loans.

This signals that the borrowers entering the pipeline are typically:

- Motivated

- Qualified

- Already interested in refinancing

They simply need the right loan officer to guide them through the decision process.

Low Cost Per Acquisition

Campaign data also shows that cost per acquisition is among the lowest in the industry, allowing lenders to scale campaigns while maintaining strong ROI.

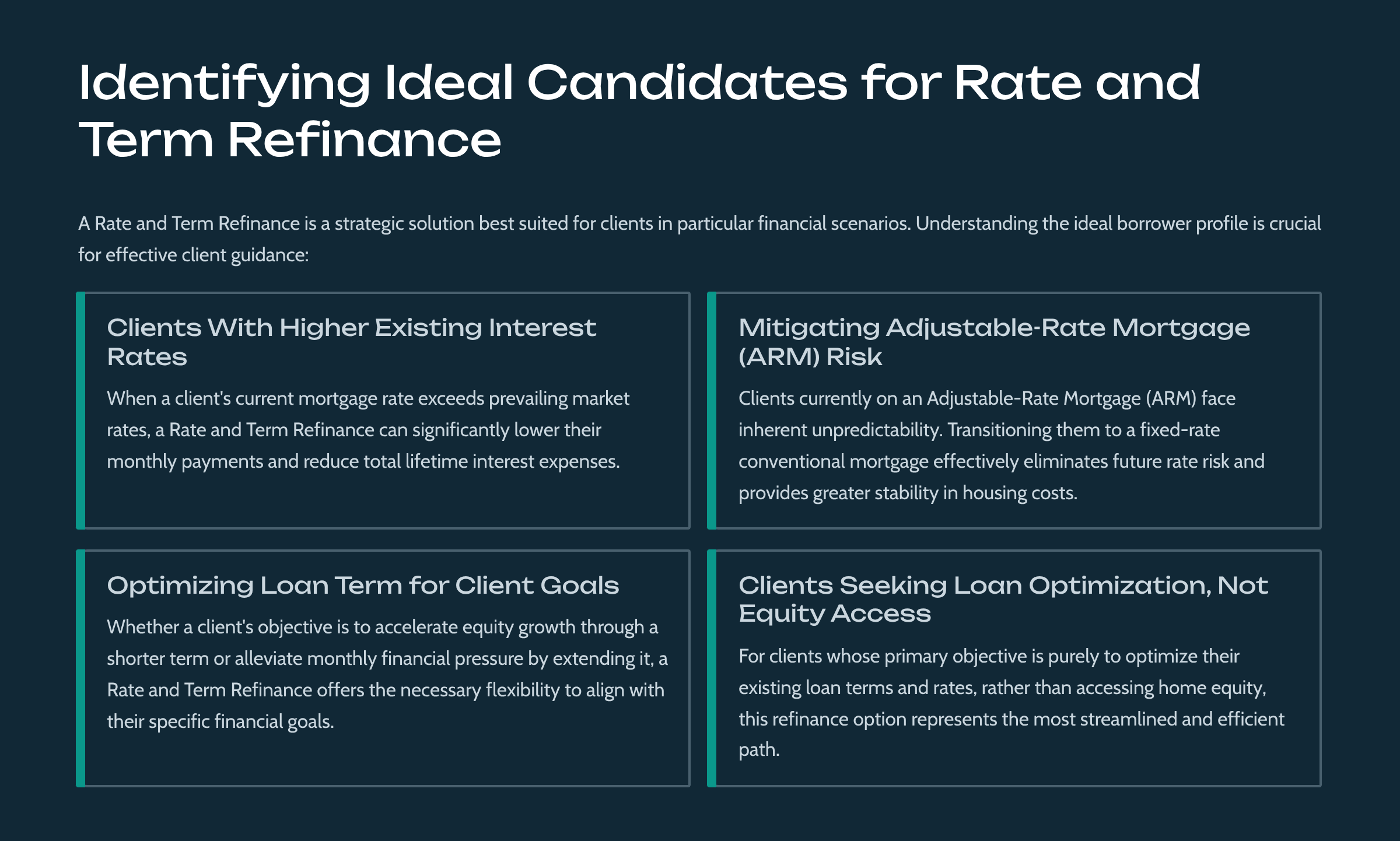

How Loan Officers Can Identify Ideal Candidates

Rate & Term Refinance is not the right solution for every borrower—but it’s extremely powerful when used strategically.

Here are some of the most common ideal borrower profiles.

Homeowners With Higher Existing Rates

If a borrower’s current mortgage rate is significantly above today’s market rates, refinancing can deliver meaningful savings.

Borrowers With Adjustable-Rate Mortgages

ARMs create uncertainty for many homeowners.

Refinancing to a fixed-rate mortgage eliminates future rate risk and stabilizes housing costs.

Clients Looking to Optimize Their Loan

Some borrowers want to:

- Shorten their loan term to build equity faster

- Extend the term to lower monthly payments

A Rate & Term refinance allows flexibility to meet these goals.

Borrowers Focused on Loan Optimization (Not Equity)

For homeowners who don’t want to tap home equity, this refinance option is often the most streamlined solution.

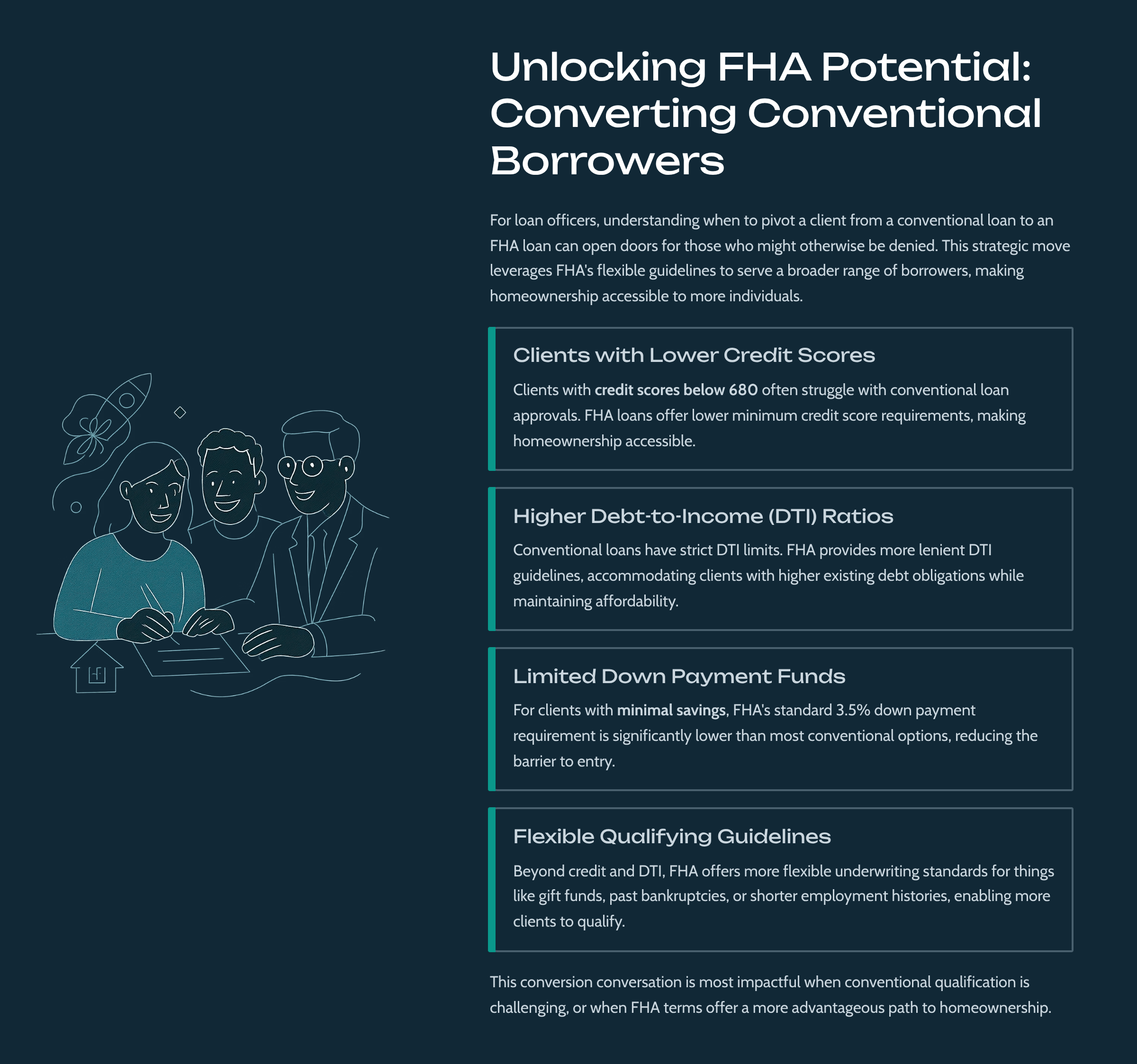

When FHA May Be a Better Path

In some cases, borrowers pursuing a conventional refinance may benefit from switching to FHA guidelines instead.

Loan officers often pivot to FHA when borrowers have:

- Credit scores below ~680

- Higher debt-to-income ratios

- Limited cash reserves for closing

- Non-traditional income or employment history

FHA’s more flexible underwriting guidelines can help expand approval opportunities and keep deals moving forward.

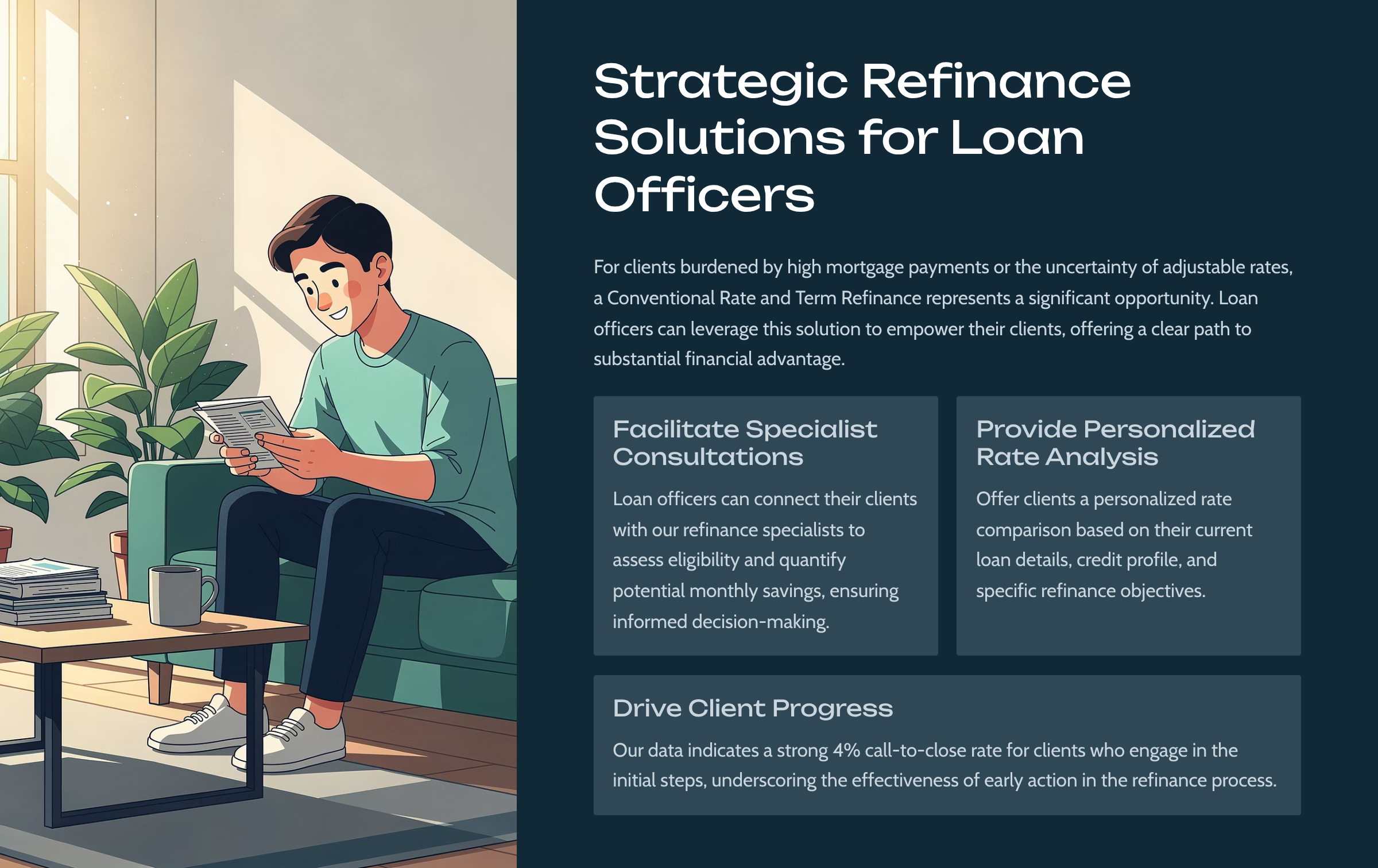

Turning Refinance Opportunities Into Closed Loans

For loan officers, the key to converting refinance opportunities is early engagement and expert guidance.

Successful lenders typically focus on:

Personalized Rate Analysis

Providing borrowers with clear comparisons between their current loan and potential refinance options.

Specialist Consultations

Connecting borrowers with refinance specialists to evaluate eligibility and projected savings.

Proactive Outreach

Identifying borrowers who could benefit from refinancing before they begin shopping elsewhere.

With a 4% call-to-close rate, the data shows that the consultation itself is often the most important step in converting motivated borrowers into closed loans.

Ready to Launch Your Rate & Term Refinance Strategy?

Conventional Rate & Term campaigns are proving to be one of the most efficient refinance marketing opportunities in today’s market.

If you're a direct-to-consumer lender looking to:

- Increase refinance volume

- Generate higher-quality borrower conversations

- Lower your cost per acquisition

Our team can help you build a strategy tailored to your pipeline.

Talk to Your Account Manager

Reach out to your Monster Lead Group account manager to:

- Identify your best Rate & Term candidates

- Optimize your refinance pipeline

- Launch targeted campaigns built for today’s market

See Full Presentation Below